The Next AI Trade

And how to take advantage

TLDR: Today we dive into our most speculative research piece yet, taking a look at why the strongest trade we’ve seen in two decades is slowing and what can be expected next. We make a parallel to another significant cycle in the last 20 years… and its not the one you think.

We lay out the facts, our interpretations, our insights into what comes next as well as a deep dive into a new investment that we believe has multibagger potential in the years ahead.

For many investors, recent months have been boring at best, awful at worst.

Its been very bad for the high beta riders (most influencers, lazy substack researchers, etc… who have just taken advantage of markets drunk to the brim on risk in 2025 that forgot to sell and are now almost all underwater), but it has also been weak for many disciplined investors who have been tracking large macro trades.

The reality is that the top level trade that has dictated market movements from the top down for the last ~3 years is coming to and end: The Traditional AI Trade.

The long compute/capex trade was great for the last three years, led by Nvidia, Broadcom, and newer names in novel fields like Lumentum but also by firms deemed long term AI winners such as Google.

And from a financial perspective it is still thriving.

Hyperscalers guided for capex in 2026 that blew by any and all street estimates (a lot of it healthily funded through FCF for now) and Nvidia presented a strong beat and raise last week, showing that their business may actually be re-accelerating.

The issue here in recent months hasn’t been fundamentals, even the largest companies in the world look cheap:

The Hyperscaler lot is trading at some of their lowest relative valuations ever, outside of Google who seems to have firmly put itself in the lead of the AI race in recent months.

On the other hand:

Semis, while obviously the incumbent market leaders, are well off their valuation peaks, with Nvidia trading all the way down to a forward PE of below 20x and a PEG of <1… remarkably cheap.

The natural question for researchers and prospective investors here now is why is this happening across the market amongst the largest companies that have led a strong market regime for three years?

It comes down to the Capex Cycle:

This chart posted by Michael Burry does a good job in explaining a lot of whats happening here.

On one hand you have hyperscalers investing mind numbing amounts of capital into the compute buildout, with the largest names plowing their entire FCF for 2026 back into capex. This creates immense uncertainty, and while for the most part these firms have shied away from bond markets to fund these investments, it looks like a bygone conclusion that we will see many debt raises in the coming months as FCF is finite but so far the demand for inference compute is infinite. Its hard to get bullish on a company spending at these breakneck paces, even if it is certain that the technology is likely going to be extremely value-additive.

That takes you to the other side, those receiving this capex like Nvidia.

In theory, if these companies are continuing to pour hundreds of billions of dollars into capex the beneficiaries will be semis, hardware providers, etc… but investor psychology on the flip side is that everyone knows its a capex CYCLE. Eventually these immense investments will come to an end, and even though its clear that it won’t in the next six months, what isn’t clear is just how fast it will when it does.

What happens to semis when we reach enough compute to power the ultimate ML models that don’t need further training or are at a level of capability that they can begin to improve themselves faster and more efficiently?

We saw a preview of this in early 2025 with Deepseek, showcasing a model that can run on much less compute and power than initially expected.

Eventually the data centers will be built, and even if compute needs are extremely high, they won’t be infinite.

What will be damn near infinite is the demand for inference (especially if you want to replace three billion human workers like the doomers are predicting).

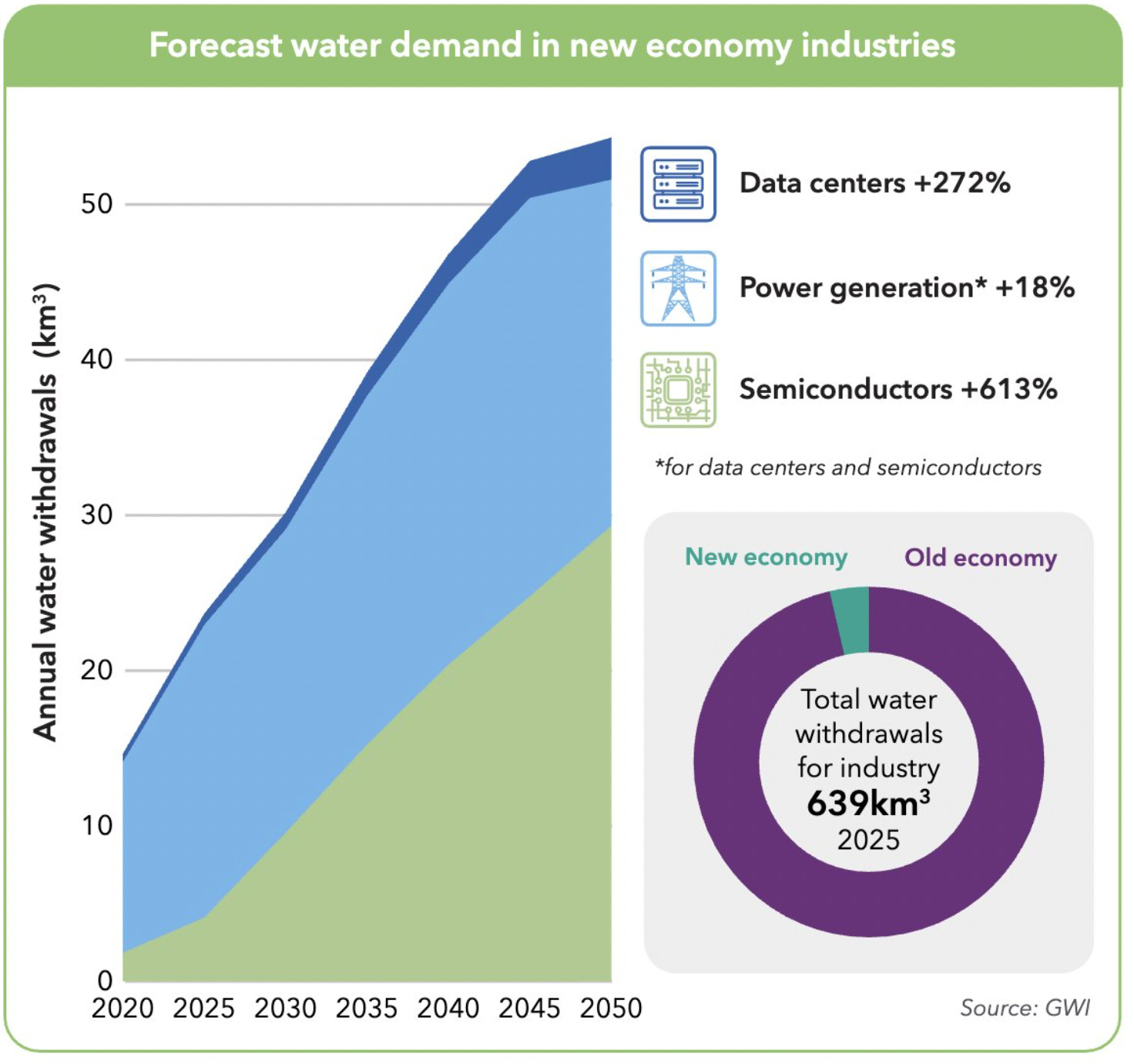

That means the focus then shifts from fixed asset investments (physical data centers and GPUs (in a longer view)) to recurring expenses which include power, water and waste. The things that ensure that inference is continuous… but sustainable.

This isn’t a new thesis, everyone knows this, power names are up hundreds of percent and we even have a standalone thesis on a separate company in this exact theme.

But we are taking a bit of a different stance here, drawing parallels to another historical cycle that followed a similar pattern of extreme capex to build a revolutionary technology. We see from the past what can happen in the future of this cycle, and what names we should further hone in on.

The dotcom bubble.

Nope.

Thats probably what you thought, and most people love to compare every single technology cycle to, but it really isn’t the same.

What is this cycle like in reality?

The shale boom.

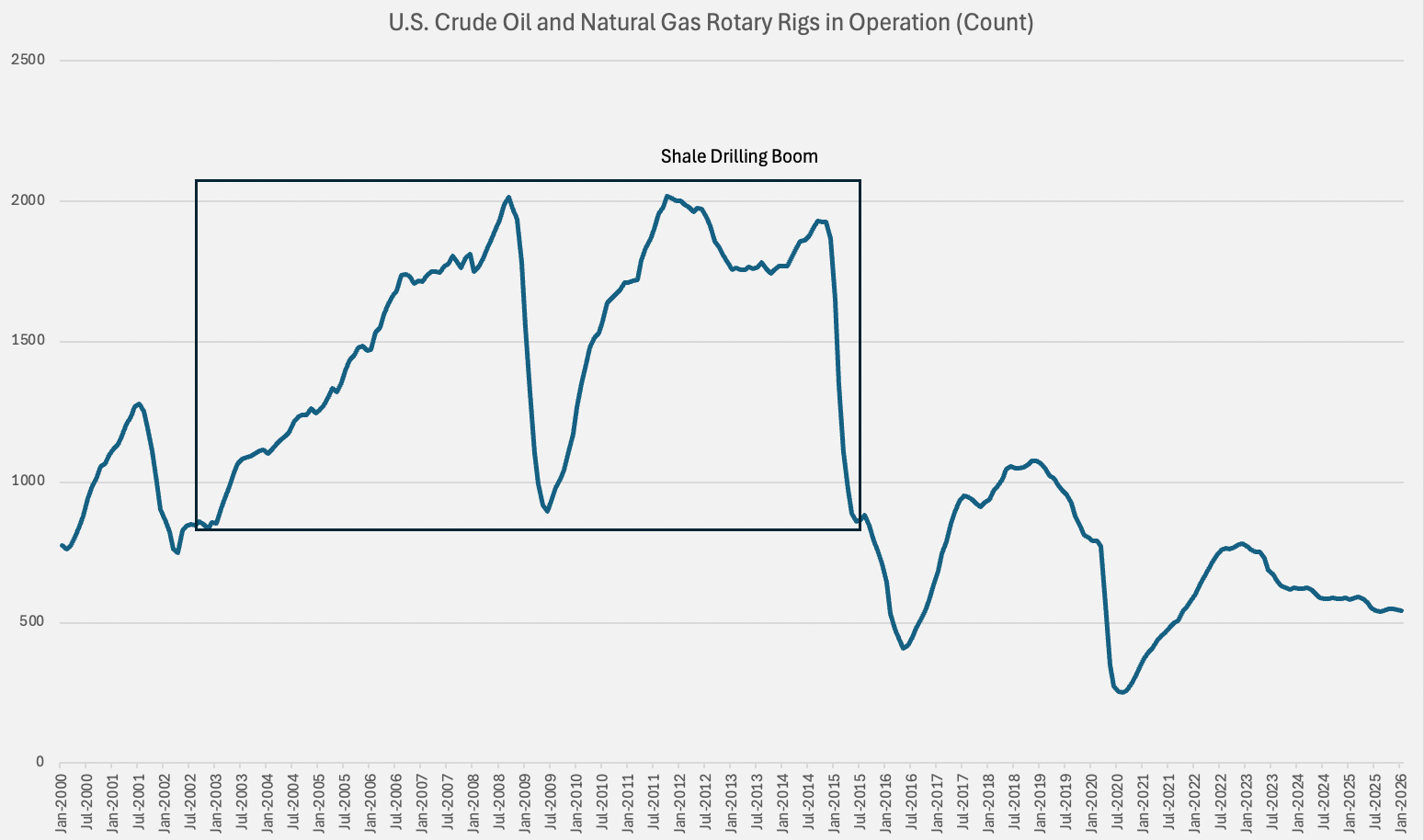

The Shale Boom: A Cycle That Rhymes

In the early 2000s, the energy industry was sitting on top of a technological revolution it didn’t fully understand yet. Hydraulic fracturing, “fracking”, had cracked the code on extracting oil and gas from shale formations that were once considered unreachable. The reserve base of the United States was being rewritten in real time. It was a genuine, civilization-altering breakthrough.

And then the capital came. In waves. In floods.

Every private equity firm, every major oil company, every wildcatter with a lease and a dream plowed money into drilling. At peak cycle, the shale patch was consuming tens of billions of dollars per year in capital expenditure. New rigs, new wells, new pipelines, new processing facilities. The buildout was staggering.

And here is what almost everyone forgets: the technology worked. Shale was not a fraud. It was not the dotcom bubble. The oil came out of the ground. American production went from roughly 5 million barrels per day to over 13 million… the single largest increase in oil production in the history of the world.

The shale revolution succeeded.

But the investors? Many were ruined.

The problem was never the technology. The problem was the capital cycle. Too much money, chasing too few truly differentiated assets, all at the same time. Producers drilled so efficiently that they collapsed their own margins. Debt-funded independents flooded the market with supply, crashed the price, and then found themselves trapped with fixed-cost infrastructure and variable-rate debt in a world where oil had re-priced.

The technology wins. The capital cycle is brutal. Many equity holders are destroyed anyway.

The companies that actually made money (durably, consistently, across the entire arc of the shale boom) were not the drillers. They were the companies providing the non-optional, recurring, consumable inputs that every single well required regardless of the oil price. The sand companies. The chemical blenders. The water disposal firms. The pipeline operators with locked contracts. The inspection and integrity businesses that kept the infrastructure running.

They didn’t need to pick the winning driller. They just needed to be in the path of the throughput.

This Is That Cycle.

Replace ‘shale fields’ with ‘data centers.’ Replace ‘GPUs’ with ‘oil rigs.’ Replace ‘training runs’ with ‘wells drilled.’ The structure is nearly identical.

The hyperscalers are the integrated oil majors, spending their entire free cash flow and then some, racing to out-drill each other in the belief that compute dominance equals market dominance. Nvidia is the premium rig manufacturer, printing money on every cycle of the buildout.

The market has priced all of this perfectly — and that’s exactly the problem.

Because here is what comes next, and this is the part of the shale story that most people skipped: after the wells were drilled, the economics shifted completely. Drilling capex slowed. What never slowed (what actually accelerated) was the demand for the inputs required to keep those wells producing. Water. Chemicals. Power. Maintenance. Disposal. The operational economy of a mature field.

We are approaching that inflection in AI. The data centers will be built. The GPUs will be racked. The training runs will complete. And then the world will need to run inference… continuously, indefinitely, at a scale that makes today’s workloads look like a prototype.

What does continuous, global-scale AI inference require?

Power. Enormous, permanent, baseload power.

Water — staggering quantities of it, for cooling systems that run 24 hours a day, 365 days a year.

And increasingly, solutions to the waste streams that this consumption produces: the heat, the water discharge, the chemical byproducts of running a civilization’s worth of compute in a building.

Power. Water. Waste.

The shale analogy tells us exactly where to look.

Not at the drillers, those trades have been made.

Look at the non-obvious, recurring, non-optional input providers. The ones whose revenue doesn’t depend on which AI model wins, which hyperscaler dominates, or whether Nvidia’s margins compress. The ones who just need the inference to keep running.

That is what we are hunting for at Krypton Research. And we think we found something genuinely extraordinary.