[Public] The Market's Truth

A note on geopolitics, and what the real next move is for markets

TLDR: Today’s piece is brought to you straight from our Macro desk, and was primarily written as an impromptu research note before markets close here for the week in a few hours. We talk about our views on the Iran situation and this morning’s surprise jobs report miss, as well as what the market is telling investors about them and how we should think about positioning moving forward.

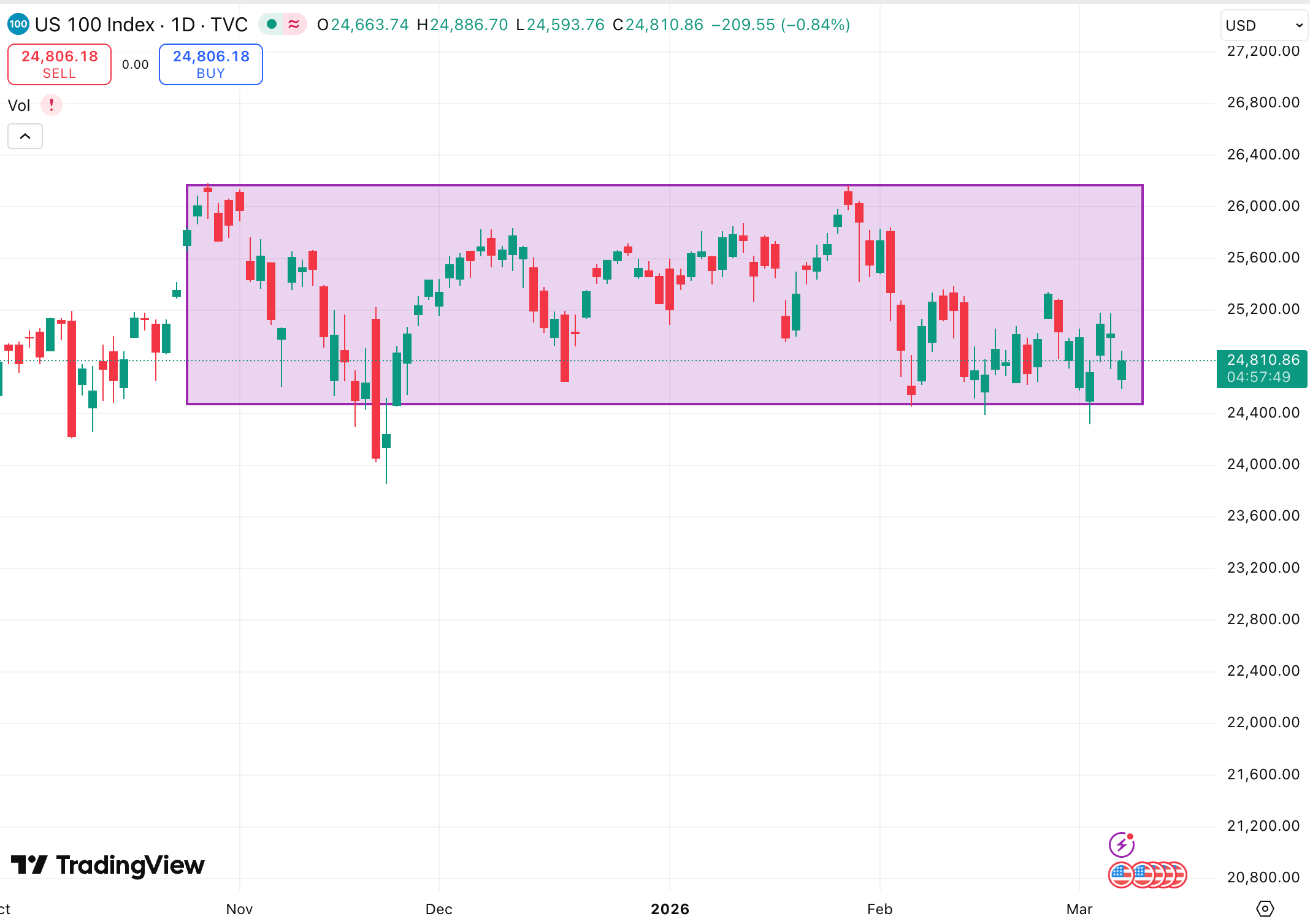

Markets have had their first “volatile” stretch of the last few months over the last two weeks:

We put volatile in quotations because if you ignore all the noise and fear mongering across social media you would see that in reality the indexes are still trading within their ranges which are now pushing nearly half a year in length.

So equities are holding up, but volatility has appeared in other ways:

Crude prices have gone vertical.

Front month WTI and Brent contracts have surged over $90 as the Iran conflict persists, with the Strait of Hormuz (carrying ~20% of the world’s oil consumption/day) remaining devoid of tanker traffic.

You also have the VIX printing just about new highs for the year dating all the way back to the tariff drawdown last April.

So there is definitely volatility, just not present in stock prices so far, and this price action in equities begins to give us hints into what the market is thinking moving forward, a thought process that we align with…

The Keys

As we head into this weekend, there are many situations to monitor, all with major macroeconomic ramifications.

Lets first take inventory of them and conclude with our overall take on how it all comes together and how we should look at markets here and handle positioning afterwards:

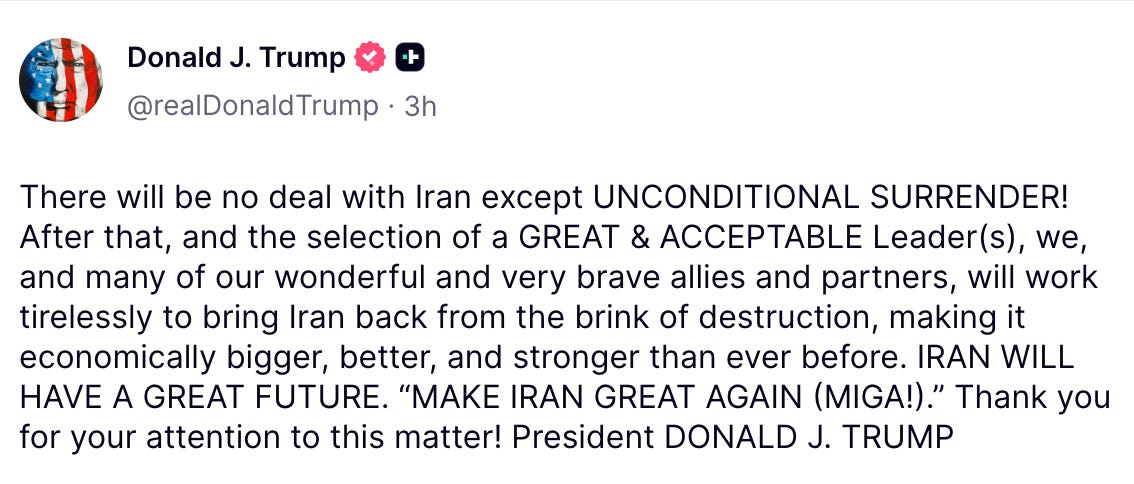

First and foremost, the Iran situation.

The United States took decisive action last weekend with strikes on Iran that effectively disposed of many of the highest ranking Iranian military leaders, including the Supreme Leader of the Islamic Republic, Ali Khamenei.

The first strike was effective, and Trump has stated many times that this operation was to go by the way of Venezuela 2.0… the issue is that Iran already possessed a host of weapons and missiles, and with the top leadership wiped out, these weapons fell into the hands of a fractured leadership, leading to chaos. Iran fired missiles and drone strikes across the Middle East and vowed to attack any ship attempting to transit the vital Strait of Hormuz.

Iran didn’t roll over or break into protests/anarchy as the U.S. would’ve wanted and the conflict has instead dragged on a full week, leading to worries of prolonged supply chain disruption, sending oil prices 25%+ higher.

This view was rectified today as Donald Trump, in the post above, said there would be no deal with Iran unless it included an unconditional surrender, signaling the chance for a more protracted conflict than expected.

This is the leading concern, and one, if it goes the way oil bulls tell you it will, that could spell disaster for global economies.

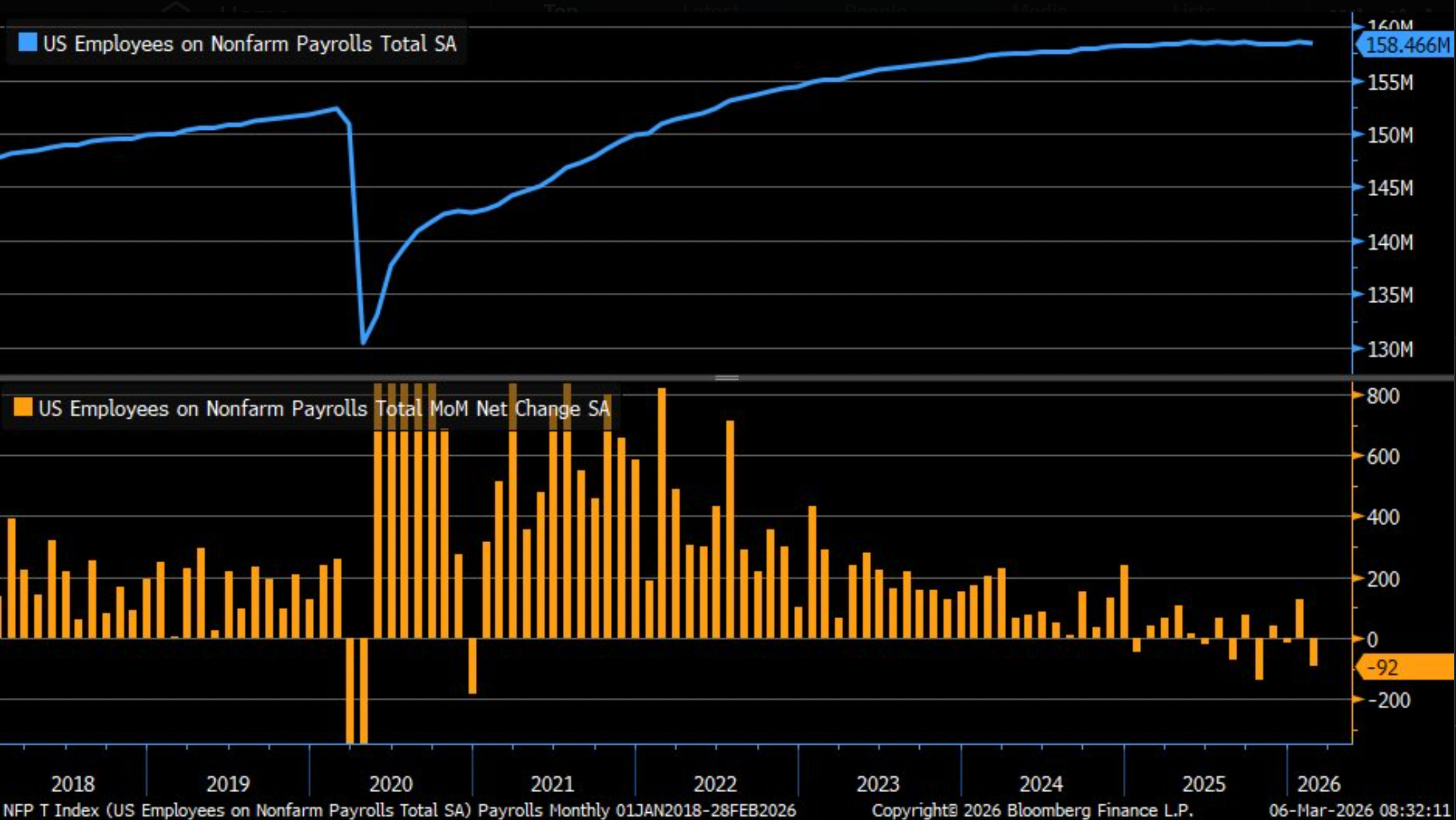

As if the Iran issues weren’t enough, this morning we got a shock labor report that saw the U.S. losing 92,000 payrolls for the month of February, an astonishing six standard deviation miss from expectations of +84,000.

This added to the already compounding fears surrounding the labor market due to the onset of AI in the workforce and began to start talks about the Fed being late to cut.

Pair weaker job growth and higher inflation led by an oil price shock and it didn’t take long for the “S” word to be floated around by social media analysts (stagflation).

Our Take

With these things in mind, we would like to spin back to the market.

The S&P500 is only 3% off its all time high and the Nasdaq is only slightly weaker at -5.5%.

But despite this “strength”:

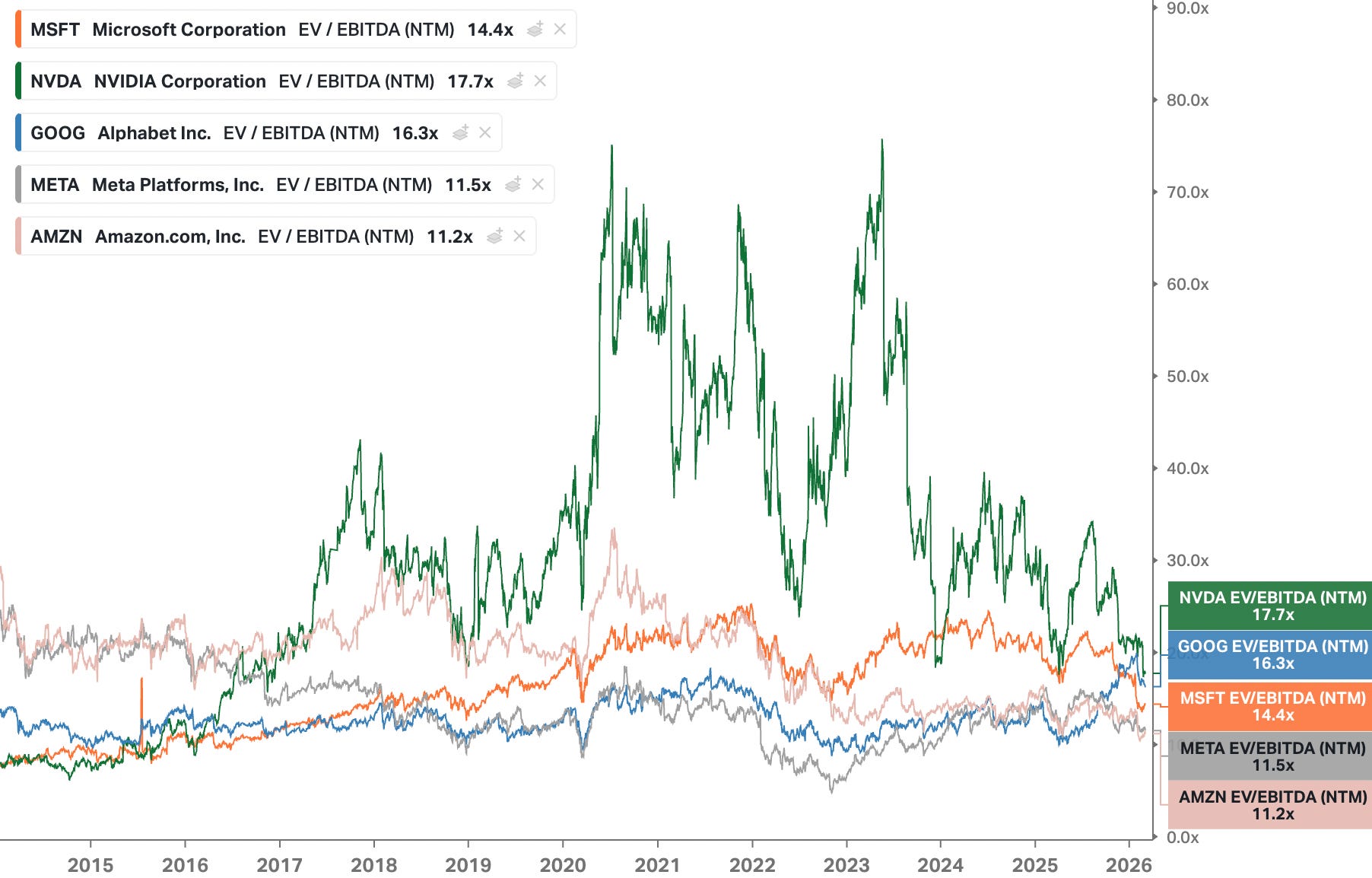

Valuations in top companies remain rooted and even cheap.

Microsoft and Amazon are now trading at their lowest valuations in nearly a decade and the broader “Mag7” basket has shown weakness in recent months as market breadth expanded outside of the extremely concentrated basket.

This rotation and breadth expansion has allowed indexes to stay flat, even through drawdowns of -30% in Microsoft and -20% in Amazon as well as deep corrections in Nvidia and Meta.

On top of this:

Market participants are heavy in puts and other hedges.

To an unprecedented level.

Crashes don’t happen when everyone expects them, and while the argument is there that this time is different and there are very real geopolitical concerns that can upend the global economy… how real are they?

Front end futures markets are notoriously volatile, so taking the current oil price spike at face value is futile since they can just as easily open -20% Sunday evening on any resolution.

Whats more important is digging deeper into what is actually going on:

Global oil prices are reacting to the Hormuz closure as a simple supply shock to global balances… but thats not really how oil markets work.

In reality, one must examine where these crude and LNG flows are ending up, which refineries and who stands to lose the most:

Ding Ding Ding

China.

More than a third of all the Oil flowing through the strait goes to Chinese refineries.

And who happens to be pretty much the only nation in the world who could slightly have Iran’s back? Also China.

As far as the U.S. economy goes, we have more than enough oil and future oil flows to sustain ourselves and mitigate direct price increases.

Many oil pundits will try to lure you astray by signaling that the U.S. produces predominantly light sweet crude while the middle east is dominated by the heavier, sour, oil… conveniently forgetting two of the largest heavy crude producers in the world being Canada and our newly “owned” Venezuela. Both firmly in our ally circle and sphere of influence.

While China has stockpiled oil reserves over the last few years, a prolonged supply disruption would spell economic disaster for the country (well before it would for the United States).

So just from a geopolitcal standpoint, China will not allow Iran to maintain this closure of the strait, and even if they only allow Chinese tankers to flow through this instantly takes the closure from a 100% close down to a 65% closure overnight… a vastly different proposition for the global supply/demand for oil.

And Iran has no choice but to listen to China.

90% of Iranian oil goes to China as well, which is pretty much the only thing that is keeping the whole of the Iranian economy alive.

Both Iran and China need the Strait more than the United States does.

But thats the geopolitical view.

How about just militarily?

Iran Missile launches during the first 8 days of conflict: (Observed, Unofficial)

Day 1 — 350

Day 2 — 175

Day 3 — 120

Day 4 — 50

Day 5 — 40

Day 6 — 32

Day 7 — 28

Day 8 — 15

The trend is obvious, and it makes sense.

There is no real leadership or organized strategy currently in Iran and they are simply firing off whatever they can at whoever they can.

No serious money manager or analyst will buy into a fear-based scenario that Iran seriously has any military capabilities to survive a conflict lasting more than a couple more weeks.

In our view, the U.S. takes decisive action this weekend, as Trump has no other option given oil prices, to swiftly end this war and at the very least maintain oil throughput in the strait.

All this leads us to the conclusion that despite surging oil, record bearish positioning and a dismal jobs report, if the market can maintain a simple -3% downside move, its is overwhelmingly likely that we see a 10%+ move to the upside in the coming months as conflict resolves and the Fed begins cutting rates again after a period of pause.

Our views on geopolitics shift to bearish oil, and that the oil market has gone offsides in bullish positioning, overestimating Iran’s ability to meaningfully impede global oil supply and under-appreciating the China angle.

In fact, there is a higher chance that we see oil prices set new lows after this conflict under the scenario that the U.S. can successfully get meaningful regime change in Iran, which would mean we see both Venezuelan and Iranian oil come online into the glbal market later this year (First and Third highest reserves under U.S. control and you’re bearish?)

We see valuations as ranging from reasonable to cheap across the largest companies and with grander and grander bear scenarios failing to disrupt price action in any meaningful way, the market is basically signaling exactly whats going to happen, especially when you realize that all these negatives are likely short term at best.

We maintain a bullish stance, expect a grind higher in indicies into Q1 earnings season in May. Take advantage of near term volatility to add to positions in top conviction names like the ones we have covered.