[Public] The Final Frontier

A basket of stocks for the next global theme

Editors Note: This research piece was first published to paid subscribers on March 15th, 2026. Our entire basket of 6 stocks covered in this piece has returned an equal-weight return of 46% over the last two months, outperforming the index UFO 0.00%↑ by 23% in the same period.

Here are the individual returns:

RKLB 0.00%↑ +81%

IRDM 0.00%↑ +73%

MTRN 0.00%↑ +55%

YSS 0.00%↑ +42% (Peaked 100%+)

VOYG 0.00%↑ +24%

TDG 0.00%↑ -1%

A simply remarkable set of returns, especially when the index tracking specifically space names underperforms by more than half.

The thesis laid out here remains in tact.

We will regularly make paid research reports public after some time as deemed appropriate to showcase the value provided by our analysts at Krypton Research.

TLDR: This is a special piece. We take a look at the next global theme, similar to the AI wave that has taken over markets for the last three years. In a way, we see AI as more of an accelerant theme, something that will allow for faster innovation in independent fields, just as the internet gave way to immense efficiencies in the late 90s. The next big themes will use AI as a catalyst for growth… just like this one:

Space.

We take a look at the space economy, one that will undoubtedly grow into the largest part of human growth within our lifetimes, and initiate a basket of stocks that we believe will be the best investments in the infant stages of this likely decades long trade.

On a clear night in southern Texas, a 400-foot tower of stainless steel lifts off the pad, rattles the earth for miles, and lands itself back on its launch mount like a magic trick.

You’ve seen the clips. Everyone has.

SpaceX has become the most impressive company in the world in terms of pure engineering execution. Over 200 Falcon 9 launches. Starship catching itself mid-air. A Starlink constellation that blankets the planet. Revenue reportedly north of $15 billion. And now, after two decades as a private company, Elon Musk has confirmed what the market has been waiting for.

SpaceX is going public.

Reports point to a mid-2026 listing targeting a valuation of approximately $1.5 trillion, with a raise exceeding $30 billion. That would make it the largest IPO in history, surpassing Saudi Aramco’s 2019 offering.

Let that sit for a second.

The largest IPO in history is going to be a space company.

Now, we’re not going to sit here and tell you to wait for that IPO and buy the stock. By the time SpaceX hits the public markets, every pension fund and index shop on the planet will be reaching for exposure. The price will reflect that.

What we are going to tell you is what happens around a SpaceX IPO.

When a $1.5 trillion company enters the public markets in a sector that most institutional investors have never had to seriously cover, the entire supply chain gets discovered. Sell-side coverage expands overnight. Funds that previously had zero space allocation suddenly need it. And the smaller names, the ones that actually make the stuff that goes into these rockets, satellites and defense platforms, get repriced in sequence.

This is the window.

Similar to the AI trade, the last comparable global theme, that started with the obvious winners like Nvidia getting bid up and making their move… way back in 2023-2024 for the most part. Winners didn’t just stop then and there. Names like $FIX, $LITE, $BE, and on an on made multibagger moves years after OpenAI initiated the AI trade in late 2022 with the launch of ChatGPT, and that cycle is probably not even done yet.

Themes take place in waves. Not all at once.

The space trade will be very similar to close out the decade.

SpaceX is the headliner, the Nvidia if you will, but there will be tens of other winners, many of which the market may not even realize have anything to do with space, just like no one assumed Comfort Systems ($FIX) had anything to do with AI… until it went 10x. These are the names we want.

And like every other Krypton Research piece, we are not going to find these names by screening for “space” in a Bloomberg terminal.

We are going to find them by starting from the science and working backwards.

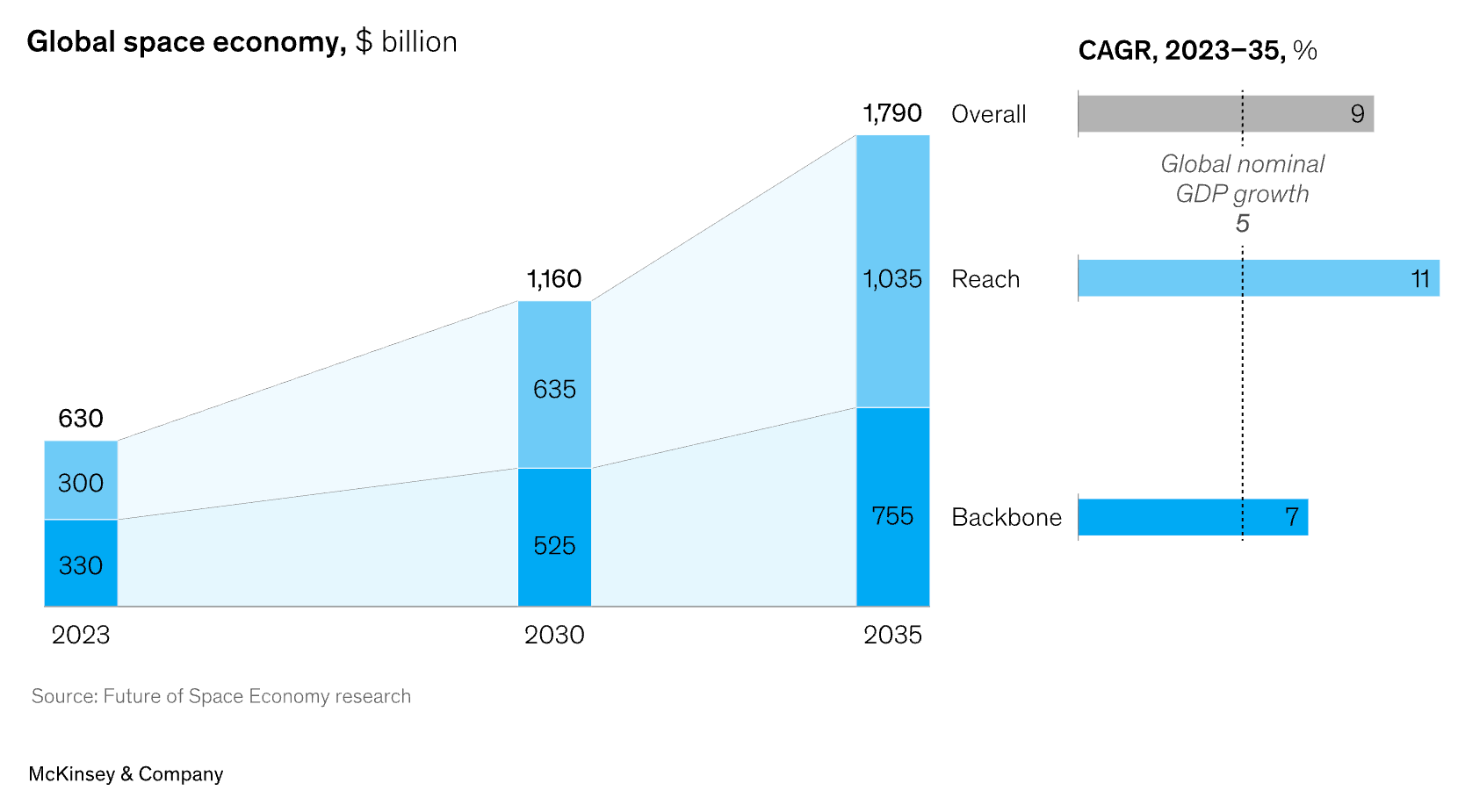

The global space economy is projected to nearly triple from roughly $630 billion in 2023 to $1.8 trillion by 2035, according to the World Economic Forum and McKinsey. That is roughly twice the rate of global GDP growth. The drivers aren’t speculative. They are satellite broadband, LEO constellations, missile defense proliferation, GPS-alternative positioning, and the early stages of in-space manufacturing and orbital infrastructure.

There is a supply chain here. And most of it is publicly traded, thinly covered, and mispriced.

We scanned the full stack of the space economy, from raw materials to orbit, and identified six names across three segments that we believe are positioned to outperform as the space economy enters its institutional phase. We have divided them as follows:

Segment 1 — The Inputs Layer. The materials and components that go into everything. Win regardless of who wins the launch wars.

Segment 2 — The Builders. The companies assembling the satellite buses and spacecraft that will populate LEO and beyond.

Segment 3 — The Operators. The companies that launch things and keep them talking. Network-effect businesses with moats that took decades to build.

None of these names were found by screening a space ETF. Most of them aren’t in one. They were found by working backwards from physics and materials constraints to the publicly traded companies that control those bottlenecks.

Lets get into it.

Segment 1: The Inputs Layer

Before a single rocket leaves the pad, before a satellite is assembled, before a missile guidance system is tested, someone has to provide the raw materials and components that make all of it physically possible.

This is the inputs layer. And it is, in our view, the safest way to play the space economy.

The logic is straightforward. It does not matter who wins the launch wars. It does not matter which satellite prime gets the next DoD contract. It does not matter if SpaceX or Rocket Lab or Blue Origin dominates the next decade. All of them need the same materials. All of them need the same components. And in many cases, there is exactly one place to buy them.

Qualification lock-in is the moat here. When a material or component gets certified for use on a defense or aerospace platform, it stays on that platform for its entire lifecycle. Switching costs aren’t economic, they are regulatory and physical. You cannot swap out a beryllium mirror for an aluminum one because it’s cheaper. The physics won’t allow it. You cannot replace a sole-source actuator mid-program because the qualification process alone takes years.

This is the kind of moat that doesn’t show up on a balance sheet but determines who gets paid for decades.

Two names here. One is a monopoly on a critical material. The other is a toll booth across the entire aerospace supply chain.

Materion Corporation (MTRN)

The Beryllium Thesis

Price: $135.99 | Market Cap: $2.8B | Analyst Coverage: 4, Consensus Target $178

Krypton Research: Bear: $174 (+28%) | Base: $241 (+77%) | Bull: $330 (+142%)

There is a metal that is six times stiffer than steel at one-third the weight, maintains dimensional stability at extreme temperatures, and is transparent to X-rays and certain wavelengths critical for space-based optics.

It’s called beryllium.

And there is one Western company that controls the full supply chain from mine to finished component.

Materion Corporation.

This is not a competitive advantage built on brand, distribution, or even patents. This is a competitive advantage built on geology and physics. Beryllium is rare, toxic to process (requiring specialized facilities and handling), ITAR-restricted, and designated as a critical material by the U.S. Department of Defense.

The barriers to entry aren’t just high.

They are effectively infinite for any realistic competitor in the Western world.

Every high-precision satellite optical system, every missile guidance component, every space-based sensor suite that requires dimensional stability under thermal extremes needs beryllium. And Materion is the only meaningful domestic source.

Now here is where it gets interesting from an investment perspective.

The market does not price Materion as a space and defense monopoly. The market prices it as a diversified specialty chemicals company. And because of that classification, Materion trades at a significant discount to what the business actually is.

The company reported FY2025 revenue of approximately $1.79 billion with net income of $74.8 million. The real story is forward looking. Management issued 2026 earnings guidance of $6.00 to $6.50 per share, sitting on top of a stronger profit base driven by higher-value engineered products and margin expansion in aerospace and defense end markets. KeyBanc recently reiterated their Buy rating and raised their price target to $170.

But the valuation tells the real story.

Materion currently trades at roughly 13x NTM EV/EBITDA. The specialty chemicals median, sits at approximately 13.4x. Its clear what the market thinks Materion is…

As every major space program scales, whether it is Starlink V3, Golden Dome missile defense, or the next generation of GPS satellites, beryllium demand scales with it. And every gram of it flows through Materion.

The re-rating catalyst is straightforward. As the space economy enters the institutional spotlight, analysts will be forced to re-examine what Materion actually is. When they do, a specialty chemicals multiple on a defense monopoly will not hold.

We model a bear case of roughly $174 (current multiple holds, modest growth), a base case near $241 (re-rating to peer median on guided earnings), and a bull case approaching $330 (full aerospace/defense premium with accelerated space demand).

Obviously these are likely conservative, but its hard to model just how fast and when these massive re-rating moves happen, but one thing is clear, there will be no space economy without the materials provided by Materion.

Only four analysts cover this stock. That alone tells you the market hasn’t found it yet.

Key Risks: Concentrated exposure to cyclical semiconductor and industrial end markets alongside aerospace/defense. A short order book reduces near-term visibility. China tariff dynamics remain a wildcard for margins.

TransDigm Group (TDG)

The Toll Booth Thesis

Price: $1,214.66 | Market Cap: $68.6B | Analyst Coverage: 22, Consensus Target: $1,594

Krypton Research: Bear: $1,150 (-6%) | Base: $1,590 (+31%) | Bull: $1,900 (+56%)

If Materion is the monopoly on a single critical material, TransDigm is the toll booth across the entire aerospace supply chain.

TransDigm makes the unglamorous stuff. Actuators. Ignition systems. Fluid connectors. Cockpit components. Hydraulic valves. Seat belts. The things that no one thinks about until they fail, which is why they never get replaced. (Sounds like $RRX?)

Approximately 75% of TransDigm’s sales are sole-source, meaning once a TDG part gets specified into an aircraft platform, commercial or military, it stays on that platform for the life of the program. These are not commodity parts. They are proprietary, highly engineered, FAA/DoD-certified components that took years to qualify. The switching cost is not a price comparison. It is a multi-year re-certification process that no OEM or airline wants to go through.

This creates an economic profile that is absurdly good. TransDigm reported Q1 FY2026 (quarter ending December 2025) net sales of $2.285 billion, up nearly 14% year over year. EBITDA as defined was $1.197 billion, representing a 52.4% EBITDA margin. Read that again. A 52% EBITDA margin on an aerospace components business.

The full-year FY2025 revenue came in at $8.83 billion, up 11% from the prior year. Earnings grew 26% to $1.87 billion. Management raised FY2026 guidance following Q1 results.

So why is this in our space basket?

Two reasons.

First, TransDigm’s products are already on virtually every military and commercial aerospace platform that interacts with the space economy. Every satellite deployment vehicle, every defense platform integrated into missile warning systems, every aircraft that supports space operations carries TransDigm components. As the defense budget around space grows, particularly with programs like Golden Dome ($151 billion in projected spending), TransDigm’s existing installed base collects more revenue.

Second, TransDigm has been flat to down over the past year while the rest of the aerospace and defense sector has run 40 to 150%. The reason is mechanical, not fundamental. Boeing and Airbus OEM destocking created a temporary revenue overhang as production schedules slipped. This is a transient dynamic. As OEM production normalizes through 2026 and 2027, the structural earnings power of the business reasserts.

The consensus analyst price target sits around $1,590, representing approximately 30% upside from current levels. 13 analysts rate it a Buy.

The space economy buildout is incremental TAM on top of an already dominant compounding machine. TransDigm does not need space to work. But space will make it work even better.

Key Risks: OEM production delays extending beyond current expectations. High leverage (net debt to EBITDA typically runs elevated). Rare earth supply chain disruptions have been flagged as a near-term headwind. Premium valuation relative to industrial peers, though justified by margin profile.

Segment 2: The Builders

Materials go in. Spacecraft come out.

This segment is about the companies that are actually assembling the satellite buses and spacecraft components that will fill low Earth orbit and beyond over the next decade. These are the primes and near-primes of the new space economy, the firms taking raw materials, components and IP and turning them into the physical hardware that gets launched.

Both names here share important characteristics. Both are thinly covered. Both have structural contract lock-in with the U.S. government. Both are pricing in execution risk that, in our view, the backlog data does not support.

The market is treating these companies like speculative bets. The order books tell a very different story.

York Space Systems (YSS)

The Broken IPO Thesis

Price: $19.81 | Market Cap: $2.5B | Analyst Coverage: 10, Consensus Target $38

Krypton Research: Bear: $29 (+46%) | Base: $38 (+92%) | Bull: $55 (+178%)

York Space Systems went public on January 29, 2026, pricing its IPO at $34 per share. It opened at $38. And it has been grinding toward all-time lows ever since, currently sitting roughly 44% below its first-day high and near its all-time low of ~$20.

The market repriced it like a speculative new issue from a hot sector that got ahead of itself.

The business underneath is not speculative.

York is one of the primary contractors for the U.S. Department of Defense’s Proliferated Warfighter Space Architecture, which is the Pentagon’s constellation-based approach to missile tracking and communications in LEO. Their S-CLASS satellite bus platform is essentially the Foxconn model for military satellites. Standardize the structure, scale the production, compress unit economics. The company wins approximately 83% of the contracts it bids on and currently produces an estimated 14% of all U.S. military LEO satellite production.

Think about that for a second. A company that wins 83% of its bids and holds 14% of DoD LEO satellite production is trading at its all-time low.

The revenue trajectory supports the thesis. Through the first nine months of 2025 (the latest available pre-IPO financials), York posted roughly 59% year-over-year revenue growth. The company has approximately 670 employees and a vertically integrated production line designed specifically for volume satellite manufacturing.

The catalyst here is earnings. York’s first public earnings report is scheduled for March 19th, 2026, covering the full fiscal year. When the backlog converts into reported numbers, the speculative IPO overhang should begin to lift.

Golden Dome is the demand accelerant. The $151 billion missile defense initiative relies heavily on LEO satellite constellations for tracking and communication, directly in York’s core competency.

The analyst consensus is overwhelmingly positive. Ten analysts cover the stock with a consensus price target of $39, representing approximately 92% upside from current levels. JP Morgan initiated coverage with an Overweight rating in late February.

At a price-to-sales ratio of roughly 7x on trailing revenue, York trades below the peer group average of approximately 11.3x for comparable space and defense primes. This is a company growing revenue at 59% that trades at a discount to its sector.

The broken IPO dynamic is one of the most reliable setups in small-cap investing. When a strong business IPOs into a weak tape and gets repriced on sentiment rather than fundamentals, the rubber band eventually snaps back. We believe York is that setup.

Key Risks: Pre-earnings uncertainty (no public quarterly results yet). Concentrated government customer base means budget and shutdown risks are real. The stock has limited trading history, which amplifies volatility. Lock-up expiration could add near-term selling pressure.

Voyager Technologies (VOYG)

The Hidden Asset Thesis

Price: $27.02 | Market Cap: $1.6B | Analyst Coverage: 7, Consensus Target: $43.43

Krypton Research: Bear: $18 (-33%) | Base: $44 (+63%) | Bull: $55 (+104%)

Voyager Technologies makes star trackers, radiation-hardened laser communications systems, missile guidance components, and advanced navigation solutions for defense and space applications.

That alone would make it an interesting small-cap defense play.

But Voyager is also building Starlab, a commercial space station, as a NASA-backed joint venture. And the market is essentially giving you that option for free.

Let’s break down the math.

Voyager ended 2025 with $491.3 million in cash and cash equivalents. With approximately 59.5 million shares outstanding, that is roughly $8.25 per share in net cash sitting on the balance sheet, supported by IPO proceeds, preferred stock, and convertible notes.

At a current price around $27, you are paying roughly $18 to $19 per share for the actual operating business.

That operating business just posted a record year. Full-year 2025 revenue was $166.4 million, up 15% year over year. The year-end backlog hit a record $265.6 million, up 33% from the prior year. Defense and National Security revenue grew 63% in Q4 alone.

And management just raised 2026 revenue guidance to $225 to $255 million, representing 35% to 53% year-over-year growth. Off a record backlog.

The market originally tried to label Voyager as a single-contract defense company with NGI (Next Generation Interceptor) concentration risk. The most recent earnings call dismantled that narrative. Only 25% of the $200 million defense backlog is tied to NGI. The rest is diversified across multiple programs.

Then there is Starlab.

Starlab recently completed its commercial Critical Design Review, a significant maturity milestone that validates the program’s readiness to move into full system procurement and development. Voyager also recently made a strategic investment in Max Space for expandable habitat technology tied to NASA’s Artemis program. These are not PowerPoint visions. They are funded, advancing programs with a major government partner.

Seven analysts cover the stock with a consensus price target around $44, representing roughly 63% upside from current levels. All seven rate it a Buy. The most recent Q4 results missed Wall Street’s estimates slightly, but the raised guidance and record backlog tell a more important story.

The thesis here is simple. You are paying $18 per share for a defense business growing 35 to 53% off a record backlog, and you are getting a commercial space station program as a free call option.

Key Risks: Still loss-making. The company posted a $116 million net loss for full-year 2025, with negative adjusted EBITDA and negative free cash flow. Starlab is capital-intensive with execution risk. Government shutdown uncertainty is a near-term overhang on revenue guidance. The stock remains volatile and thinly traded.

Segment 3 — The Operators

Materials get processed into components. Components get built into spacecraft. Now somebody has to put them in orbit and keep them communicating once they’re there.

This is the operations layer. The companies that actually launch hardware into space and maintain the networks that make orbital infrastructure useful. These are network-effect businesses. The moats are not built on patents or branding. They are built on physical infrastructure that took decades and billions of dollars to deploy, and cannot be replicated quickly by anyone.

One of these is priced as a speculative growth story with the fundamentals already backing it up. The other is priced as a legacy telecom company when it is actually one of the most strategically valuable communications assets on Earth.

Rocket Lab (RKLB)

The SpaceX Analog Thesis

Price: $68.41 | Market Cap: $38.8B | Analyst Coverage: 15, Consensus Target $90

Krypton Research: Bear: $45 (-35%) | Base: $69 (+1%) | Bull: $110 (+61%)

Rocket Lab is the only company outside SpaceX with a proven, repeatedly flying orbital rocket.

SpaceX = $1.5T | Rocket Lab = $40B

The closest analog/competitor to the biggest IPO ever trades at a 97% discount.

In a world where dozens of launch startups have burned through billions in venture capital trying to reach orbit, Rocket Lab has flown 83 missions on its Electron rocket, including 21 launches in 2025 alone with a 100% success rate for the year. They have already launched four missions in 2026, including executing two launches in six days from two different countries.

This is not a concept. This is an operating business at scale.

And the launch business is actually the smaller part of the story.

Rocket Lab’s Space Systems division, which encompasses satellite design, spacecraft manufacturing, optical systems, star trackers, and on-orbit management, is rapidly becoming the core growth engine. The company was awarded its largest single contract to date in 2025, an $816 million prime contract with the Space Development Agency for missile-tracking satellite constellations. Backlog reached a record $1.85 billion at year end, up 73% year over year, with management indicating 37% of that backlog is expected to convert within the next twelve months.

Full-year 2025 revenue hit a record $602 million, up 38% year over year. Q4 alone delivered $180 million in revenue with record 38% GAAP gross margins. Management guided Q1 2026 revenue of $185 to $200 million, sustaining the acceleration.

Then there is Neutron.

Neutron is Rocket Lab’s medium-lift rocket currently in development, targeting the $10 billion-plus per year medium-lift launch market that is currently served almost exclusively by SpaceX’s Falcon 9. A stage one tank test failure caused a delay, pushing the expected first launch to Q4 2026. This is a risk, but it is an engineering problem, not a fundamental one. The tank design has been reworked and manufacturing fixes are in place.

Neutron is effectively a free call option on top of the already-growing Electron and Space Systems business. If it works, Rocket Lab becomes a genuine second option for medium-lift launch services globally. If it is delayed further, the base business continues to compound.

But the real catalyst for RKLB is not Neutron. It is SpaceX.

When SpaceX files for IPO, Rocket Lab is the first name institutional investors reach for to get public market exposure to the space launch economy. There is no other comparable liquid, pure-play space launch and systems company at this scale. That positioning alone justifies paying attention to RKLB ahead of the event.

The valuation is not cheap. At roughly 46x 2026 estimated revenue, Rocket Lab is priced for continued high growth execution. This means the upside is not in consensus. It is in the tail scenarios that Wall Street is not modeling for now, primarily Neutron success, accelerating SDA contracts, and the SpaceX IPO halo effect.

Key Risks: Pre-profitability. Net losses continue as R&D investment in Neutron scales. Neutron delays are the most obvious overhang. Valuation is demanding by any traditional metric. SpaceX itself is a competitor across launch and space systems, which could cap pricing power long-term.

Iridium Communications (IRDM)

The Misclassified Asset Thesis

Price: $24.86 | Market Cap: $2.6B | Analyst Coverage: 9, Consensus Target $29

Bear: $17 (-32%) | Base: $31 (+25%) | Bull: $49 (+97%)

This is the name on this list that most people will scroll past. And that is exactly why it is here.

Iridium is not a satellite phone company.

It is a 66-satellite low Earth orbit constellation providing the only truly global, pole-to-pole communications coverage on the planet. Not even GPS covers the entire globe. Iridium does. Maritime vessels in the Arctic, aircraft over the Pacific, military units in remote theaters, IoT sensors on oil rigs in the middle of nowhere. If you need a signal where no other signal exists, you use Iridium.

The financial profile is quietly exceptional. Full-year 2025 revenue was $871.7 million, up 5% year over year. Operational EBITDA came in at $495.3 million, also up 5%, representing a 57% OEBITDA margin. Net income was $114.4 million. The company generates approximately $296 million in annual free cash flow.

Read those numbers again and then remember the market cap is $2.5 billion.

That is roughly an 11% free cash flow yield. On a subscription-based, recurring-revenue satellite communications monopoly. With 2.54 million billable subscribers and growing.

The market files Iridium under “legacy telecom” and applies a distressed multiple because the name evokes the original Iridium that went bankrupt in 1999. That Iridium and this Iridium share a name and a constellation. They share nothing else. This business was restructured, recapitalized, and has been generating enormous free cash flow for years.

The 2026 guidance is modest by design. Management guided flat to 2% service revenue growth and OEBITDA of $480 to $490 million, reflecting a $17 million headwind from shifting incentive compensation entirely to cash. This is conservative corporate guidance, not a growth problem.

The real catalysts are forward looking.

First, the Satellite Time and Location (STL) service is expected to launch in mid-2026. This is a GPS-alternative positioning chip that provides timing and location data via Iridium’s constellation, offering a backup to GPS in environments where GPS is jammed, spoofed, or unavailable. In a world where electronic warfare is increasingly targeting GPS signals, this is not a niche product. It is a national security priority. And it represents a genuinely new revenue stream for a company the market has already written off as ex-growth.

Second, Iridium Certus broadband services continue to grow into maritime and aviation markets, providing high-bandwidth connectivity in regions where geostationary satellites cannot efficiently serve.

Third, and perhaps most importantly, CEO Matt Desch has signaled openness to a potential sale of the company. If the space economy enters an institutional re-rating cycle driven by the SpaceX IPO, an asset like Iridium, irreplaceable constellation, massive free cash flow, recurring revenue, defense applications, becomes an obvious acquisition target.

We model a bear case of roughly $17 (growth stagnation, no multiple expansion), a base case near $31 (modest re-rating to reflect FCF generation and new revenue streams), and a bull case approaching $49 (full re-rating as a space infrastructure asset or takeout premium). The current price of $24 represents meaningful upside to even the base case.

Iridium’s projected cumulative free cash flow from 2026 through 2030 ranges from $1.5 to $1.8 billion. The entire enterprise value today is roughly $4.5 billion. You are buying this for less than three times the cash it will generate over the next five years.

Nine analysts cover the stock. The consensus price target is around $29 depending on the source, with a high of $40. Morgan Stanley recently lifted their target to $26 while maintaining an Equal Weight rating.

Key Risks: Low near-term growth. The 2026 guidance of flat to 2% service revenue growth will not attract momentum investors. Competition from Starlink and other LEO broadband constellations could erode pricing power at the margins over time. The constellation is aging (launched 2017-2019) and a next-generation replacement will eventually require significant capital expenditure. SoftBank-esque risk does not apply here, but general space sector sentiment could drag shares if the SpaceX IPO disappoints.

Closing Thoughts

Six names. Three segments. One thesis.

The space economy is about to go from a niche sector to an institutional asset class, and the clock is the SpaceX IPO. When a $1.5 trillion company enters the public markets, the entire supply chain gets repriced. Sell-side coverage expands, index funds need exposure, and the names that were too small or too boring or too “off the beaten path” for Wall Street suddenly become discovery stories.

We found these six names by doing what Krypton Research always does. We started from the science. We mapped the physics. We worked backwards through the materials and components. And we arrived at the publicly traded bottlenecks that Wall Street has not yet connected to the space economy story.

To be clear, these are not all new portfolio positions for Krypton Research. We are not blindly adding six names to the book at once. This is a curated basket, a thematic watchlist of stocks that we have vetted through our research process and believe will outperform as the space economy scales.

We present them here as a framework for our readers. This is how we thought about the space economy. This is the supply chain map we built. And these are the six names that survived the filter.

We’ll keep a tracking of this basket under the name KSP (Krypton Space), to go along with our existing tracking of both the KEW (Krypton Equal-Weight) and KMF (Krypton Managed Fund). The benchmark index for KSP will be $UFO.

Some of you may want broad exposure and can build a small position across all six. Others may gravitate to a specific segment, whether that is the safety of the inputs layer, the asymmetric upside in the builders, or the network-effect moats in the operators.

In the future, we may go fully in depth on one of these names and initiate it as a formal portfolio position, once we clear out room from our current picks.

For now, these are our horses in the space race.

The window to be early closes fast. Position accordingly.